Command Palette

Search for a command to run...

ChatGPT Boasts Hundreds of Millions of Users, but Its Paid Conversion Rate Is Less Than 10%. How Can AI Be Converted Into Sustainable Profits?

Since 2025, the "gap" between massive investments in artificial intelligence and commercial returns has increasingly become a focus of public opinion. On the one hand, global tech giants continue to bet on AI infrastructure and algorithm development, endorsing AI as the engine of the next industrial revolution; on the other hand, capital markets, macro analysts, and independent observers have also begun to closely monitor the stock performance of AI companies.

Taking the US market as an example,NVIDIA's stock price repeatedly hit new highs in 2025.This reflects investors' enthusiasm for its AI chip business; while companies like Microsoft, Google, and Meta performed strongly overall, their gains showed structural differences, with some sectors facing increased pressure for correction. In the Chinese market, Alibaba's stock price hit a multi-year high this year, and AI-related stocks such as Tencent and Baidu also performed actively, demonstrating the market's continued focus on the localization of AI applications and infrastructure. Overall,Global capital markets continue to price the AI industry at a relatively high level.This background has become an important premise for the current discussion on the "AI bubble".

Media outlets and think tanks worldwide have bluntly stated that many AI companies have yet to establish a robust profit model. While massive capital expenditures may boost valuations in the short term, they may not necessarily translate into sustainable profits. Meanwhile, financial reports from major companies show that AI investments have profoundly impacted profit margins and cash flow performance, prompting the market to seriously question whether large investments yield large returns. Some commentators have even likened the current wave of AI investment to a historic gamble; if the returns fail to materialize, its scale and impact will be no less than that of the dot-com bubble. Against this backdrop,The evaluation of AI investment and business returns has shifted from technological elitism to a pragmatic financial review, which primarily focuses on the two core sectors of B2B and B2C that bear huge amounts of capital.

The Dilemma of Hundreds of Billions in AI Investment: B2B Returns Are Being Systemically Diluted

The global enterprise (ToB) AI market in 2025 is witnessing an asymmetrical cycle of "investment-profit." Tech giants like Amazon and Google, leveraging their capital and technological advantages, are making massive investments, yet they are trapped in a predicament of "the more they expand, the more pressure they face." Their experiences confirm the harsh reality of the industry: commercial breakthroughs in ToB AI are far more complex than simply piling on computing power.

Amazon AWS: Profitability Contradiction Amidst Computing Power Expansion

As a cloud computing leader, Amazon is extremely aggressive in its investment in AI infrastructure. AWS capital expenditures are projected to reach $125 billion in 2025, primarily for expanding AI data centers and its self-developed Trainium chip series. This expansion is expected to double by 2027.

In particular, profits plummeted in the second quarter:AWS's sales increased by approximately 17.51 billion Tb/s year-over-year to $30.9 billion, while its operating income grew by less than 91 billion Tb/s to $10.2 billion. Meanwhile, its operating expenses surged to $20.7 billion, up from $16.9 billion in the same period last year.The operating profit margin narrowed significantly to approximately 32.91 TP3T, the lowest profit-to-revenue ratio since the end of 2023, and lower than the operating profit margin of nearly 401 TP3T in the first quarter.

Despite Amazon's overall Q2 results exceeding Wall Street expectations, its stock price fell in after-hours trading on the day the earnings report was released as investors focused on rising costs in the company's biggest profit engine—its cloud computing division.

Industry analysts point out that this profit compression mainly stems from increased operating expenses and infrastructure investment, including expenditures such as expanding data centers for AI and high-performance computing.

Entering the third quarter, AWS's revenue and operating income both rebounded: Amazon's overall Q3 net sales were $180.2 billion, up 131 billion Tb/s year-over-year, of which AWS revenue was approximately $33 billion, up approximately 201 billion Tb/s year-over-year, and AWS operating income also increased from $10.4 billion in the same period last year to approximately $11.4 billion.

Although AWS's profitability seems to be moving in a better direction, a comparison between Q2 and Q3 makes AWS's core problem clearer: profits do not follow a fixed upward curve, but are highly sensitive to the pace of investment, customer computing power procurement cycles, and infrastructure depreciation.When capital expenditures enter a period of high intensity, profit margins quickly come under pressure; when revenue increases in the short term while new investment slows down, profits will recover in stages.This volatility itself demonstrates that AI investment has not yet been transformed into a stable source of cash flow with "self-reinforcing capabilities".

Google Cloud: The Commercialization Myth of Full-Stack Technology

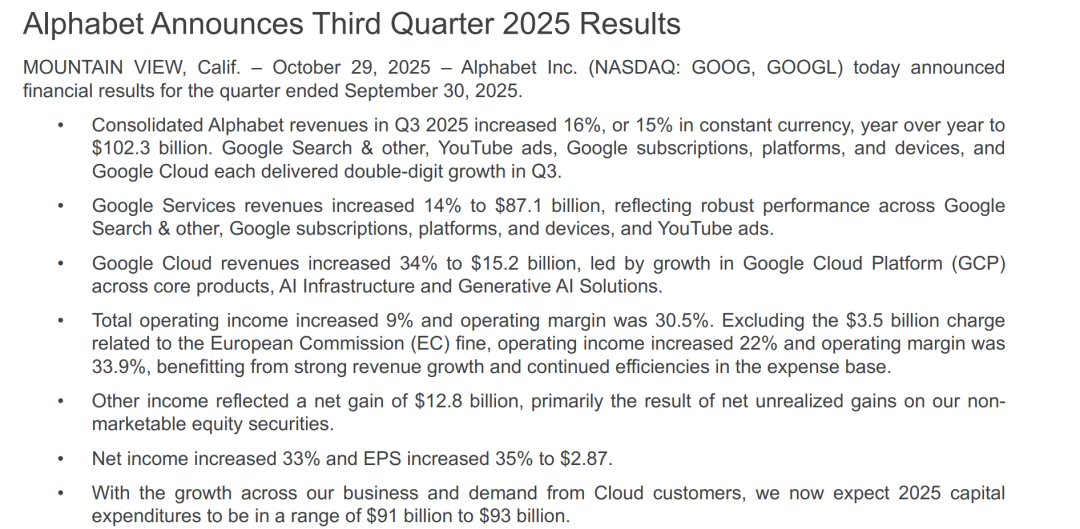

Over the past two years, Alphabet has explicitly placed AI at the core of its cloud business growth. With the full integration of Gemini large-scale models into Google Cloud and the large-scale deployment of its self-developed TPUs in data centers, Google is attempting to build a differentiated competitive advantage through its full-stack capabilities of "chips + models + cloud platform". The results show that this strategy has indeed brought significant revenue growth: in the third quarter of 2025, Google Cloud revenue reached approximately $15.2 billion, a year-on-year increase of over 301 billion TPU, making it the fastest-growing among the three major cloud vendors.

However, a deeper analysis reveals that its revenue growth has not kept pace with its return on capital. Alphabet has consistently raised its capital expenditure forecasts in recent fiscal quarters, with the market generally expecting its capital expenditures in 2025 to be close to $90-93 billion.The new investment will be mainly used for the construction of AI data centers, computing clusters, and model training infrastructure.This pace of investment is significantly faster than the pace of profit release from the cloud business, raising concerns among investors about a "mismatch between AI investment and returns."

It's worth noting that Google still has high ROI case studies. According to official reports, some companies achieved an average return on investment of 7271 TP3T within three years through Google Cloud AI, with a payback period of approximately eight months, and an average increase in productivity and output value of $205,000 per 1,000 employees.However, such cases rely on high barriers to entry: a single client must invest tens of millions of dollars upfront, data governance and model fine-tuning must take more than six months, and a dedicated engineering and consulting team is required for support.

Industry perspective: ToB AI profitability is difficult to replicate universally.

The predicaments of Amazon and Google are not isolated cases. Research from the IBM Institute for Business Value shows that only 251 TP3T of enterprise AI projects globally have achieved their initial ROI targets, with only 161 TP3T achieving large-scale, cross-departmental deployment. MIT's analysis further points out that of the $30-40 billion invested in generative AI globally, approximately 951 TP3T of projects have not yet generated quantifiable commercial returns, with only a few pilot projects creating millions of dollars in direct value.

This series of data reveals the core reality:ToB AI is not incapable of generating profits, but rather it is difficult to become a scalable profit engine.While massive capital expenditures can ensure technological leadership, the return cycle is long and the profit model is still in development. Investors and companies must face up to long-term structural risks.

ToC Sector: ChatGPT's Hundreds of Millions of Users and Monetization Challenges

If the challenge in the B2B sector lies in the "imbalance between input and output," then the challenge in the consumer (B2C) sector centers on the "disconnect between user scale and paid conversion." MIT research shows that only 5% of AI projects achieved measurable returns.Top-tier models like Google Gemini have a task completion rate of less than 31 TP3T in real-world scenarios such as medical diagnosis. If revenue cannot maintain an annual growth rate of 100 TP3T over the next 2-3 years, the probability of a bubble bursting is as high as 70 TP3T.

Consumer-grade AI products, such as ChatGPT, have rapidly accumulated users, but are encountering growth bottlenecks in the deeper waters of commercialization.

Revenue growth struggles to keep pace with computing power costs

OpenAI's annualized revenue is projected to exceed $20 billion by 2025, more than doubling from $8.5 billion in 2024. However, this growth is accompanied by an exponential increase in computing costs. According to Business Insider, ChatGPT receives over 1 billion calls per day, with monthly computing costs for inference alone reaching $320 million. Adding the $12 billion one-time investment required for training the GPT-5 model further prolongs its profitability cycle.

In fact, with OpenAI losing $12 billion every quarter and seeing almost no hope of breaking even, the AI bubble seems to have arrived, and many users are pessimistic about AI.

JPMorgan Chase's analysis further reveals industry-wide challenges:To achieve a 10% ROI, the global AI industry needs to reach $650 billion in annual revenue by 2030.This figure equates to an extra $34.72 per iPhone user per month, or $180 per Netflix subscriber per year—clearly, the current consumer market's willingness to pay is far from reaching that level.

The "glass ceiling" of paid conversions

The expansion of the user base did not lead to a corresponding increase in the paid subscription rate.

According to data shared by Sam Altman in early October 2025, ChatGPT's weekly active users had reached 800 million, an increase of 300 million users since March. Some media outlets commented that while this sounds impressive, it's likely that none of the 299 million new users will actually pay.As of Q2 2025, ChatGPT had 180 million monthly active users, but only about 15 million paid subscribers, a paid subscription rate of less than 8.51 TP3T.

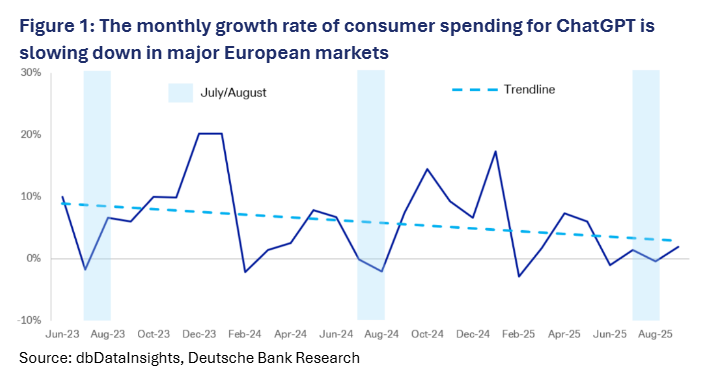

Furthermore, the situation in the European market is even more severe. According to a research report by Deutsche Bank, consumer spending in ChatGPT's five major markets—France, Germany, Italy, Spain, and the UK—has almost stagnated since May 2025. The growth of paid users may have peaked. Although weekly active users have reached 800 million, paid subscribers are only about 20 million, which is a huge gap from its $500 billion valuation.

A similar situation has occurred with enterprise-level AI office tools. For example, Notion AI quickly accumulated tens of millions of users after its launch, but its paid conversion rate has remained at around 5% for a long time. Enterprise customers mainly use free or basic packages, making it difficult to drive subscriptions for advanced features. This phenomenon shows that even if the tool has productivity-enhancing value, users still tend to "just get what they need," and paid growth is naturally limited.

The root cause of this predicament lies in the "misalignment of value perception".Consumer-grade AI products mostly focus on auxiliary scenarios such as content generation and information retrieval, making it difficult for users to perceive their core value as "essential".For example, while the AI drawing tool Midjourney has achieved annual revenue exceeding $500 million through a subscription model, it still faces the risk of user churn due to "aesthetic fatigue after frequent use." According to SimilarWeb data, in January 2024, Midjourney's organic search traffic was 18.37 million, but its unique visitors were only 7.39 million, a decrease of 5.91 TP3T. Its overall and access data directly reveal that its retention rate remains a major weakness. Meanwhile, AI chatbots are caught in the awkward situation of "sufficient free features and lackluster paid features," struggling to break through the "glass ceiling" of paid conversion.

The Homogenization Trap in Business Model Exploration

Currently, the monetization paths for ToC AI are highly concentrated, and a differentiated competitive landscape has not yet formed. Looking at mainstream products, business models mainly fall into three categories:

Subscription model:For example, ChatGPT Plus and Gemini Advanced rely on high-frequency user payments, but face the risk of "churn of price-sensitive users";

Advertising monetization:Some AI social products generate revenue through in-feed ads, but balancing user experience and commercialization is extremely difficult and can easily provoke user resentment.

Contextualized payment:AI video editing tools that charge based on export duration and AI writing assistants that charge based on word count may match the usage scenarios, but they have low average order value and limited user lifetime value.

This homogeneous exploration leads to "involutionary competition"—of the more than 120 new consumer AI products launched globally in 2025, 83% adopted the "free + subscription" model, ultimately falling into a vicious cycle of "relying on subsidies to grab users and relying on price increases to retain users," making it difficult to form a sustainable profit model.

Reconstructing the Long-Term Ledger of AI Amidst the Metamorphosis of the "Bubble"

Faced with the dual growing pains of the B2B and B2C sectors, the "AI bubble" seems to have become an inescapable shackle of the times. In an interview in November, Google CEO Sundar Pichai also clearly stated the reality of the AI bubble and admitted that "if the AI bubble bursts, I don't think any company will be spared, including ourselves."

However, simply equating this short-term imbalance between investment and return with "technological failure" and classifying AI investment as a "bubble" clearly ignores the development pattern of disruptive technologies.The current predicament is temporary rather than fundamental. The underlying logic and long-term value can only be clearly understood by reconstructing and evaluating the financial statements.

First, for tech giants like Google and Meta, AI investment is essentially a "defensive survival investment" in response to industrial transformation, rather than a simple "profit-seeking" endeavor. The core reason for the imbalance between investment and return lies in the fact that their primary goal is not to generate marginal revenue, but to build a technological moat. If their core businesses, such as search and social media, are severely impacted by AI, their existing profits of hundreds of billions will instantly collapse. This "life-saving tax" attribute explains why these giants continue to aggressively increase their investment even when their financial reports are under pressure. Short-term profit pressure is a way to avoid the risk of being eliminated in the long term, which is one of the core logics of long-termism.

Secondly, the essence of AI is the "commodification of intellectual labor," and its value release model is destined to differ from the traffic monopoly of the early internet era. The failure of commercial returns to meet expectations largely stems from the market's misjudgment of AI's profit model. When technology drives a 50-100 fold leap in productivity, previously scarce professional skills will rapidly depreciate, and AI will transform from a "scarce tool" into "infrastructure." This attribute determines that AI is unlikely to replicate the excessive monopoly profits of the early internet era; its generated value will rapidly spread across the entire industry, transforming into a universally beneficial cost-based capability, rather than a moat for a single enterprise. Therefore,Assessing the value of AI should not be limited to the short-term revenue of a single company, but should focus on its long-term contribution to improving the efficiency of the entire industry chain.

Furthermore, the value realization of AI follows a typical "J-shaped curve," and is currently in the trough of the transition from the "investment phase" to the "explosive phase." OpenAI CEO Sam Altman has pointed out that the commercialization of generative AI requires a long period of infrastructure construction, during which the investment and return will inevitably be extremely asymmetrical; Nvidia CEO Jensen Huang has also emphasized that...Current computing power expenditures should not be viewed as traditional operating expenses (OpEx), but rather as upfront capital costs of the "new production function".This means that short-term losses are not a sign of "no hope of return," but rather a necessary accumulation before the technology matures.

Conclusion: The "Non-linear" Oscillations of the AI Commercialization Curve

The current asymmetry between investment and returns in the AI industry is not due to the failure of the technology itself, but rather an inevitable consequence of commercialization failing to keep pace with the speed of technological iteration. Just as the evolution of disruptive technologies such as electricity and the internet has shown, AI will also go through a cycle of "massive investment - model adjustment - value explosion," and the current profitability dilemma is an unavoidable growing pain in this cycle.

The ToB profit model is difficult to replicate on a large scale and has a long return cycle, while the ToC user scale is disconnected from paid conversion and the business model is homogeneous and competitive. The dual challenges of the two tracks have jointly fueled the controversy of "AI bubble". However, the research reports of Sequoia Capital and a16z have already pointed out the core: the so-called "bubble" is just the market's excessive expectation of short-term arbitrage, rather than a disproving of the long-term technological potential of AI.

This predicament more clearly reveals a key reality: the commercialization curve of AI is still in a difficult formative stage—the underlying basic capabilities are still being developed, the granularity of industry scenarios needs further refinement, and users' understanding of AI needs to gradually evolve from "a dispensable auxiliary tool" to "a native flow embedded in production and life." Therefore, the clamor of the "AI bubble theory" has not diminished its core commercial value; on the contrary, it signifies that the industry is moving from the fervor of "technological romanticism" to a mature transformation towards "pragmatic implementation," undergoing a perilous leap from "capability accumulation" to "profit realization."

After the dust settles from the expansion of computing power and the short-term arbitrage frenzy subsides, only those players who cut through the bubble and noise, adhere to long-termism, cultivate vertical scenarios, and refine sustainable profit models will be able to truly reap the ultimate fruits of technological innovation in the business civilization reshaped by AI.

Reference Links:

1.https://hbr.org/2025/11/ai-companies-dont-have-a-profitable-business-model-does-that-matter

2.https://www.reuters.com/technology/google-parent-alphabet-misses-quarterly-revenue-estimates-2025-02-04/ 3. https://nypost.com/2025/02/05/business/google-slammed-with-200b-stock-hit-over-ai-spending-fears-slowing-revenue-growth/

4.https://www.ibm.com/cn-zh/think/insights/realize-roi-ai-agents

5.https://www.geekwire.com/2025/amazon-web-services-profits-squeezed-as-ai-arms-race-drives-spending-surge